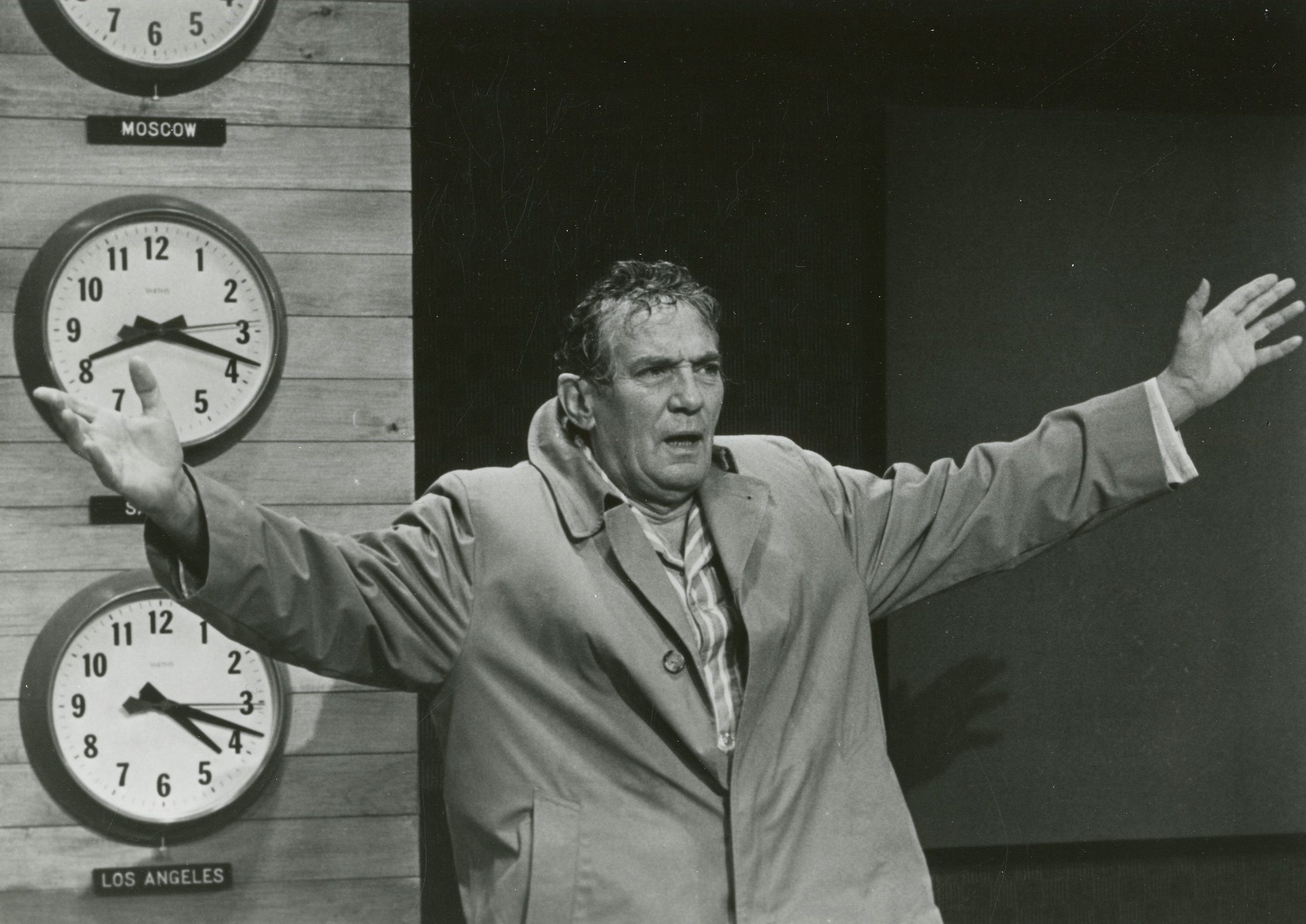

A famous scene in Sidney Lumet’s Network (1976) has grown more illuminating with each passing decade. Arthur Jensen (Ned Beaty), chairman of a multinational corporation, summons Howard Beale (Peter Finch)—the television anchor-man whose public breakdown has unexpectedly turned him into a truth-teller—and delivers what is perhaps the defining monologue of twentieth-century political cinema. Although the Cold War still frames the film’s horizon, Jensen already speaks from within the ideological universe that would soon crystallise as neoliberal globalisation. His is the voice of capital itself, transfigured into historical necessity and invested with the authority of a secular religion:

You have meddled with the primal forces of nature, Mr. Beale, and I won’t have it! … The Arabs have taken billions of dollars out of this country, and now they must put it back! It is ebb and flow, tidal gravity! It is ecological balance! You are an old man who thinks in terms of nations and peoples. There are no nations. There are no peoples… There is only one holistic system of systems, one vast and immane, interwoven, interacting, multivariate, multinational dominion of dollars…. It is the international system of currency which determines the totality of life on this planet. That is the natural order of things today. That is the atomic and subatomic and galactic structure of things today! …. You get up on your little twenty-one-inch screen and howl about America and democracy. There is no America. There is no democracy. There is only IBM and ITT and AT&T and DuPont, Dow, Union Carbide, and Exxon. Those are the nations of the world today. What do you think the Russians talk about in their councils of state—Karl Marx? They get out their linear programming charts, statistical decision theories, minimax solutions, and compute the price-cost probabilities of their transactions and investments, just like we do. We no longer live in a world of nations and ideologies, Mr. Beale. The world is a college of corporations, inexorably determined by the immutable bylaws of business. The world is a business, Mr. Beale. It has been since man crawled out of the slime. And our children will live, Mr. Beale, to see that perfect world in which there’s no war or famine, oppression or brutality—one vast and ecumenical holding company, for whom all men will work to serve a common profit, in which all men will hold a share of stock, all necessities provided, all anxieties tranquillised, all boredom amused.

Like any ideological text, Jensen’s speech is simultaneously true and false. It captures capital’s historical tendency to dissolve political boundaries and subordinate states to the imperatives of accumulation. And it also presents this historical process as a law of nature, as though the eclipse of democratic sovereignty by corporate power were simply destiny. This is ideology’s peculiar genius: it reveals reality precisely by mystifying the forces that produce it.

A generation later, Andrew Dominik’s Killing Them Softly (2012) returns to precisely the same theme, now stripped of the grand metaphysical rhetoric that still animates Jensen’s speech. The film ends with Jackie Cogan (Brad Pitt) in a bar, watching Barack Obama’s victory address on television. Obama invokes the familiar liturgy of American exceptionalism—“to reclaim the American dream... that, out of many, we are one.” Cogan’s brief monologue is devastating in its cynicism:

My friend, Thomas Jefferson is an American saint because he wrote the words “All men are created equal”—words he clearly didn’t believe since he allowed his own children to live in slavery. He was a rich white snob who was sick of paying taxes to the Brits. So, yeah, he wrote some lovely words and aroused the rabble and they went and died for those words while he sat back and drank his wine and fucked his slave girl. This guy wants to tell me we’re living in a community? Don’t make me laugh. I’m living in America, and in America you’re on your own. America’s not a country. It’s just a business. Now fuckin” pay me.

If Jensen speaks in the voice of global capital, Cogan speaks in the voice of neoliberal subjectivity. The former announces the dissolution of nations into the world market; the latter its subjective correlate, the dissolution of solidarity into social Darwinism. Between them, the ideological trajectory of the last half-century is complete: politics gives way to management, citizenship to competition, while the social bond itself is reduced to a transaction.

The architecture of financial power

Today the United States remains the world’s dominant power because it operates as the political headquarters of a globally hegemonic financial system that intersects both military power and the technological infrastructure. Politicians, in this context, are middle management technocrats, administering decisions whose strategic coordinates are established not through democratic deliberation but through the imperatives of liquidity, debt management and asset preservation.

Donald Trump’s return to power offers a textbook illustration of this situation. His campaign was bankrolled by a rogue’s gallery of billionaires, corporate predators, and sovereign wealth funds—Elon Musk, Timothy Mellon, Miriam Adelson, and a flood of Gulf petrodollars. They shared no coherent philosophy, only a singular appetite: the restructuring of the American state for their own enrichment. Trump was never chosen for his political talents—he has none. He was chosen in the knowledge that his theatrical volatility can be easily weaponised. In this respect, he is the perfect frontman for a transition in which uninhibited spectacle has finally swallowed strategy, and politics has become pure performance for an audience of creditors.

Here we should be careful not to commit the liberal’s favourite error: mistaking the puppets for the puppet-master. Yes, billionaires buy politicians—this is not news—but the rot goes much deeper. The real foundation of American financial power is the exorbitant privilege of the US Treasury securities as the world’s “risk-free” reserve asset; a confidence trick upon which the entire post-Bretton Woods order depends. Faith—often coerced—in American debt (US public debt current sits at a record $39.4 trillion, with the government debt-to-GDP ratio hovering at approximately 122.6%) allows Washington to spend with impunity, wage war, break international law without penalty, and inflate financial assets. Wall Street, the Fed and the state machinery recycle dollars into a self-reinforcing circuit of liquidity creation, asset inflation, military projection, and monetary hegemony. It is a loop that feeds on its own momentum—and woe betide anyone who dares question its sacredness.

However, this carefully designed architecture is now showing visible signs of strain. Rising Treasury yields (higher refinancing costs), persistent fiscal deficits, de-dollarisation initiatives and the growing willingness of major trading powers to settle energy transactions outside the dollar all point towards the gradual unravelling of the post-1971 monetary order built on fiat currencies decoupled from gold and propped up by US firepower. None of these developments signals an imminent collapse of American hegemony. Together, however, they indicate that the financial apparatus underpinning that hegemony has entered a period of structural instability leading to implosion.

It is against this background that contemporary geopolitical conflicts become intelligible. They should not be understood simply as struggles between sovereign states pursuing national interests, but as moments within a broader reorganisation of global capital and the monetary order that has sustained it for half a century.

Jensen’s speech therefore deserves to be heard again because it gives ideological expression to capitalism’s deepest and most delusional fantasy: that history has come to an end and the rule of global capital, homed in the US, is the natural, objective, and eternal logic of the world itself. But if Jensen speaks in the voice of necessity, our task is to recover contingency. To recognise that what presents itself as the inexorable logic of finance—a secular version of what the ancients called fate—is nothing other than the historical sedimentation of political decisions, institutional manipulations, and class power.

Wealth without value

The analysis must now take a further step forward, or risk mistaking the rearrangement of power for a radical transformation of the system itself. One begins to imagine that a more balanced distribution of global influence could somehow stabilise capitalism—this is precisely the illusion we need to resist. Multipolarity is not, in itself, the solution to neoliberal globalisation. Insofar as it refuses to question the foundational categories of capitalist reproduction, it is simply the ideological form that “crisis capitalism” assumes in its current phase.

To see why this is the case, we must recover a distinction that people rarely question, and contemporary economics has almost entirely forgotten: the distinction between wealth and value. Capitalism, today, accumulates extraordinary quantities of wealth while systematically undermining the production of value. Financial assets multiply, stock markets reach record highs, property valuations inflate and sovereign debt expands. Measured in monetary terms (the ever-expanding mass of liquidity), the world has never appeared wealthier. Yet socio-economic value is neither money nor material abundance. It is the historically specific form through which human labour is socially validated under capitalist conditions. And the substance of this value, which is the lifeblood of capital itself, is living labour employed to produce commodities.

Capital can increase wealth by replacing workers with machinery, automation, and artificial intelligence, but it generates value only through the exploitation of living labour. Machines transfer value; they do not create it. Every technological leap therefore strengthens capitalism’s productive capacities while simultaneously weakening the social relation upon which capitalist accumulation depends. The moretechnologically productive capital becomes, the less capable it is of producing value as socio-economic substance—which is what condemns so-called work societies to ever increasing misery.

This contradiction sits at the heart of modernity. What changed with the microelectronic revolution of the 1970s was its historical scale. For much of the modern era, technological innovation displaced workers in one sector while creating employment elsewhere. Eventually, however, automation began eliminating labour faster than markets could reabsorb it. From that point onwards, finance ceased merely to accompany productive accumulation, and became its substitute. Credit, leverage, asset inflation and speculative finance were no longer just excesses of capitalism. They became the compensatory mechanisms—no doubt grotesquely excessive—through which capitalism deferred its encounter with its own internal limit.

Finance capitalises expectations on future valorisation. These expectations, in turn, can be multiplied virtually ad infinitum. Every anticipated income stream—rents, dividends, royalties, taxes, debt securities, stocks, derivatives, insurance contracts—can be repackaged as financial assets and turned into immediately tradable wealth. The result is an ever-expanding mountain of claims resting upon labour that has not yet occurred and never will occur on the scale required to redeem them. Fictitious capital is not fake wealth. It is a bet on future value whose realisation is less plausible with each passing day.

This is why the present crisis cannot be understood as another debt cycle or another geopolitical transition. These are symptoms of an underlying pathology which can be summed up as follows: capital has become structurally dependent on the continuous expansion of fictitious claims because the production of value itself has entered irreversible decline. What appears as financial dynamism is the management of the system’s blind and destructive impotence. Capital no longer reproduces the conditions of its own socio-economic expansion; it reproduces catastrophic conditions to postpone its own collapse.

The financialisation of everything

Financialisation is the extension of the asset form into every corner of existence. What matters is not whether something fulfils a social need, but whether it can be converted into a stream of income capable of supporting a financial valuation. Wherever predictable revenues can be extracted, an asset can be created. Wherever an asset can be created, debt can be issued against it. Wherever debt exists, new instruments can be constructed, traded, and leveraged. The result is a self-expanding architecture of fictitious capital whose growth depends upon the continuous colonisation of everyday life.

Housing offers the clearest example. A home was once primarily a place to live, a social institution embedded within communities and family life. Today it functions increasingly as an investment vehicle. As we learned in 2008, mortgages are bundled into securities, sold across global markets, and used as collateral within far larger circuits of speculation. Housing itself becomes secondary to the asset it generates. The persistent tension between the social function of shelter and the financial imperative of appreciation is not an unfortunate side effect of neoliberalism. It is the organising principle of hyper-financialised, debt-based capitalism.

The same logic has transformed healthcare. What was once conceived, however imperfectly, as a public good has become a field of financial extraction. Hospitals are acquired by investment funds, pharmaceutical companies are valued by shareholder expectations, insurance systems become opaque, and the language of care gives way to the language of return on investment. As we should have learned in 2020, patients become revenue streams, and illness becomes an asset class.

Education follows the same trajectory. Universities no longer primarily reproduce knowledge or cultivate citizenship. They manufacture indebted subjects. Student loans become financial products, securitised and sold, while education itself is evaluated less by what it teaches than by the future income streams it promises to generate. Thus, the student enters society as a bearer of debt whose future labour has already been partially appropriated. The same holds at the other end of the life cycle, as pensions are bundled into financial instruments.

Even the ordinary routines of consumption are absorbed into this logic. Credit-card balances, automobile loans, consumer finance and payday lending all become raw material for securitisation. Everyday indebtedness is transformed into tradable securities circulating through financial markets, which means that those markets profit from social insecurity.

Financialisation thus assetises social relations themselves. The home, the body, education, old age, attention, data, anticipated future behaviour—all become collateral against which financial wealth, amassed at the top, can be conjured as if from a magician’s hat. Every sphere of life is justified in its real existence only insofar as it can be transformed into an abstract monetary claim upon tomorrow.

War represents the culmination of this logic. If housing, healthcare, and education are now financial assets, war is their most spectacular expression. While rearmament is sold to the masses as the political response to an unstable geopolitical landscape, it is, above all, an enormous liquidity event for global finance. The European Union’s SAFE programme (Security Action for Europe) alone envisages up to €150 billion in common borrowing to support defence procurement; and defence exchange-traded funds are among the fastest-growing investment vehicles in European markets. What this means is that military expenditure no longer generates profits mainly through weapons manufacturers or government contracts. Instead, it generates investable financial products. Destruction itself becomes an opportunity for portfolio diversification.

The merchant of death has migrated from the factory floor to the trading desk. Bombed cities, displaced populations, shattered infrastructures, and even a 1,000-day long genocide disappear behind ticker symbols, derivatives, exchange-traded funds, and quarterly earnings reports—because the balance sheet is all that matters to the dehumanised subject of finance. Violence undergoes the same abstraction that finance imposes upon every other dimension of social life. War is financialised: its anticipated revenues are capitalised in advance, its future contracts discounted into present asset prices, its destruction transformed into collateral supporting fresh rounds of speculation.

This is the endpoint towards which fictitious capital necessarily moves. Having exhausted the productive sphere, it feeds directly upon the conditions of social reproduction itself. Nothing remains external to accumulation. Home, health, education, security, information, the natural environment and organised violence become interchangeable moments within the same cannibalising logic.

The catastrophic administration of systemic insolvency

The Federal Reserve—and, more generally, the institutions responsible for managing contemporary flows of capital—are caught in a contradiction from which there is no technical escape. They confront a choice between two poisons: 1. Tight monetary policy (higher interest rates), which threatens recession, financial instability, and an increasingly unserviceable mountain of public and private debt. 2. Loose monetary policy (lower interest rates), which inflates asset prices, fuels speculation, erodes purchasing power and deepens social inequality. Neither path resolves the underlying contradiction because neither addresses its cause.

And this framing obscures as much as it reveals. When central bankers speak of inflation, they mean the rate at which prices are rising—a statistical abstraction. What ordinary people experience, however, is not merely inflation but affordability: the actual level of prices compared to their income. The two are not the same. Inflation can be modest while affordability collapses, because wages stagnate while the cost of housing, healthcare, education and energy continues its relentless ascent. The financialisation of everyday life has ensured that the essentials of survival now appreciate faster than the wages required to purchase them. The technocratic obsession with taming inflation thus misses the point entirely (and on purpose): the problem is not that prices are rising too fast, but that living has become unaffordable for the many while remaining spectacularly profitable for the few.

This is why the system has now entered its terminal historical phase. It no longer governs growth; it governs the impossibility of growth on capitalism’s own terms. Every intervention is a kick of the can—it postpones rather than addresses or resolves the crisis. Each rescue operation merely transfers the contradiction to a higher level of indebtedness and financial dependence. What is presented as prudent economic management is, in reality, the continuous administration of systemic insolvency.

Here we can see how acceleration turns into the governing principle. Debt expands faster than production; liquidity expands faster than value; technological innovation expands faster than employment. Every apparent solution intensifies the contradiction it claims to overcome. The next interest-rate cut, when it arrives, will almost certainly be celebrated as another successful “soft landing.” Markets will rally, commentators will praise the wisdom of central bankers, and another layer of fictitious capital will be piled upon an already impossible balance sheet.

War, in this expanded sense, increasingly encompasses inflation, austerity, indebtedness, permanent surveillance, technological mobilisation and the financialisation of destruction itself. The algorithmic choreography of strikes on Iran and the carefully manufactured narratives around Hormuz are not exceptions—they are the template. Military expenditure, digital infrastructure, artificial intelligence, emergency governance, and financial manipulation now form a single apparatus whose function is less to resolve crises than to administer them.

War, in this expanded sense, is the battlefield of social reproduction. Every emergency legitimises new mechanisms of extraction; every technological innovation extends the infrastructures of surveillance and control; every financial rescue creates new opportunities for accumulation. The battlefield is no longer only a distant theatre of operations. It is also the everyday terrain on which the conditions of life itself are colonised, monetised and put to work.

This also exposes the central ideological illusion of our moment. We are increasingly encouraged to believe that salvation lies in a different geopolitical configuration: a multipolar order, digital currencies, artificial intelligence, or a new balance between East and West. These transformations are real, but in their current form they do not transcend the horizon we have been tracing. A multipolar capitalism remains capitalist. Digital money remains the monetary expression of value. Artificial intelligence cannot replace the living labour upon which value ultimately depends—it destroys it even further.

Capitalism cannot survive its present terminal crisis. The only hope we have is that the system’s catastrophic irrationality, now laid bare for all to see, might yet generate an escape route—an exit strategy from the very logic that is devouring us. The final barrier to that exit is our own delusional attachment to a collapsing constellation.

| A guest post by

|